ASTRO 2023: A Quick View from the Road

I had a plan, and then ViewRay Happened....

From the road, a few quick thoughts…

First, my news:

For 2023, I’ll be working on the ASTRO Health Policy and Government Relations Council. So for better or worse, I’m going to try to help lead where our specialty might go from a financial perspective. Think subcommittee, likely far down ladder - be realistic with expectations :)

My personal goals for the year are to help bring more of a private practice / business oriented slant to the discussions at a national level. To me, our market is changing quickly and we need to adapt - both on the workforce side of things and on payment models moving forward. Our ability to drive towards shorter treatments, at least in the US, is creating massive pressure within our field. It is important enough for me to attempt to help. We shall see.

At a minimum, I’ll learn things and I’ll see a broader perspective. As always, feel free to reach out or comment. I can’t guarantee change but I do think I can listen and help to ensure that diverse opinions are at least heard and maybe considered at some of the highest levels. I work part time so I likely have more ability to listen and consolidate thoughts than many - maybe that can be useful. I do feel confident that at least I will have direct lines of communication with some key members of leadership.

Many roads lead to finding consensus on ROCR.

Perhaps ironically or perhaps not - around midnight Monday / Tuesday AM (hours after the Plenary session) word leaked that ViewRay was going to transition from a Chapter 11 to a Chapter 7 bankruptcy - which would not be good.

Here is a basic definition of the difference: Chapter 11 is a restructuring process where the business can continue to operate. Chapter 7 is a liquidation bankruptcy where generally, the business does NOT continue to operate.

As I said here - back in July, there was real risk to any bankruptcy filing.

At that moment, there seemed to be little real concern from many physician leaders in our field. I wrote that article in response to what I thought I was lack of understanding of the significance and risk within the process.

That risk was amplified in late August with a rejection of an attempt to restructure the DIP financing. Remember, the DIP financing keeps the lights on while you navigate the Chapter 11 process. Money was running short and they asked to restructure the process - the rejection of that requested change clearly upped the risk.

And bills were piling up. Several office leases stopped August 31st. Claim’s data is interesting as well: ASTRO is out $71K and the IRS claims $776k. Losses are often broad in these events. And management of the company by consultants isn’t cheap running over 200k for a single month.

But not in the ballpark of the MONTHLY attorneys’ fees - some 740k for ONE MONTH - as I stated, these are complex legal events. (At least they bill in 6 min increments while billing ~2k per hour). I think it is good for physicians to see these types of numbers - the business world is a big place. All public information.

In the end, my understanding is no clear buyer emerged and/or time ran out. Below is just a sample of the language in the public documents from 10/2 below.

And from an Oct 5th filing:

Third, three months into the case there is no prospect for a reorganization. To date, the Landlord is unaware of any actionable bid for the Debtors’ assets or need for continued use and occupancy of the Leased Premises after October 31, 2023. In short, there is no rehabilitative purpose for these Chapter 11 Cases.

25. In the event that the Chapter 11 Cases are converted to cases under chapter 7 of the Bankruptcy Code, the Landlord understands that a chapter 7 trustee may need reasonable access to the Leased Premises to remove estate property. The Landlord will in good faith work with the trustee to accommodate reasonable access to the Leased Premises for this purpose.

I’m not a bankruptcy expert by any means, but I do think there are now real issues for the 60+ installed machines (28 in the US per ViewRay website). Service agreements run through around the 25th of October according to public posts. Beyond that date there are likely real potential issues with servicing these machines, or having parts and engineers to keep them running. Further, as before, there are real debts that will not be paid on any level.

Again, if you see something incorrect, please reach out. As always, if needed talk to real experts regarding any decisions. I’ve tried to be purposeful careful in my language due to the complexity of the event.

To me, this event drives home the context of where we sit today. The news landed during ASTRO on the evening where, just a few hours earlier the PACE-B trial results were announced - great clinical data but data that continues to place massive pressure on radiation facility proformas in the US.

It is within this context as to why I’m going to try and assist in finding out the path forward. I think it speaks to the importance of some of the issues we are seeing if you look at the business aspect of our specialty. And the ball keeps rolling down the hypofractionation hill - gaining momentum - really several of the meeting highlights reflect the tremendous pressure in this direction.

Which seems to lead to ROCR:

With respect to the ASTRO ROCR approach, I continue to lean in favor of working along this path. But as I’ve said I’d like to see ASTRO achieve a relative consensus from membership on this effort - at least 70% and likely closer to 80% for this approach to make sense. Even its “simple” approach will create true complexity during the phase in period and subsequent years post-implementation as there will be two billing approaches - an episode based approach and the continued fee for service approach for Advantage plans and private insurance plans. At least in my conversations, there is quite clear acknowledgement that this will cause significant disruption to revenue cycles.

And make no mistake about it - it is moving forward. It was announced in a ~September 18th letter to members that ASTRO was speaking with Congress on the 14th of the month. Now there is discussion that they are passing around draft legislation - this thing is moving forward. Large stakeholders have been contacted and this isn’t something they are considering at some future date. It is moving ahead along the path today. It isn’t finalized. No legislative effort is until it gets through Congress and gets a vote, but the concept is moving ahead. If you want to help shape the thing, find a voice to channel your input - that would be my suggestion.

So with that news, let’s look at the meeting from a high level.

ASTRO’s Top 10 Results:

Below are the “top 10” pre-meeting abstract - prime slots for the event. I think it is interesting and important to consider what we consider to be important and what “we” highlighted prior to the meeting:

Let’s see… quickly perusing the list… Anything technology based? Yes. The SBRT trials are tech based trials. MRI linac or Proton related? Nope. There are 3 trials looking at less fractions. One looking at dropping the need for simulation. Two trials looking specifically at SABR approaches and how to improve them. And one looking at hyperfractionation.

We do see an expansion into kidney cancer with FASTRACK II and for twice a day treatments demonstrating potential real overall survival benefit, so it is not completely one-sided towards a push for shorter but it’s pretty clear the “shorter is better” narrative remains.

I got “in trouble” for using this line previously but if protons are in need of a “win”… well, another year of our biggest meeting rolls by and I see nothing major for protons and a continued emphasis towards shorter and shorter treatments.

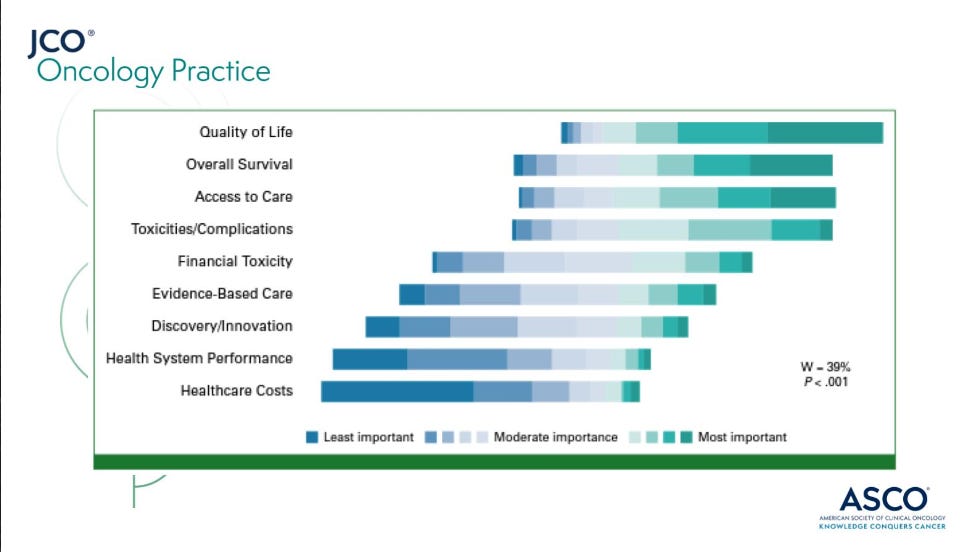

Meanwhile, down the hall, where drugs are given, costs are the last thing they consider this study:

Yet we are really fraction / cost / avoidance motivated currently. And yes, hypofractionation is applicable to several of these goals including quality of life and both clinical toxicity and financial toxicity, access to care, and healthcare costs. So the impact of less fractions is multi-factorial and therefore not simplistic to summarize into just one or even two of the above metrics - I get that.

But in radiation, over the past decade we seem to focus as much on healthcare costs and efficiency / throughput as any metric. Shorter has been a primary driver of our “progress”. And in the US, this results in a real risk of sacrificing access to care based on decreased payments with shortening of approaches. As payments shrink, centers are struggling or closing and technical innovation of our equipment is put at risk.

From my seat, rural access is changing in a rather rapid fashion (over the past decade). Empty vaults and unused machines liter Oklahoma. True stories: like strip out a few parts and then take a chainsaw to the once used equipment (literally) because it is a better business decision to simply remove it in pieces and put it in the trash rather than take on the expense to properly move it. Or consider this: In Oklahoma, multiple Cyberknife machines sit unused. (Yes they are older and towards end of life, but you can’t make this stuff up) . These machines are not being replaced, they are idle or being removed from the market.

Perhaps many will argue these facilities should have never existed and maybe that is correct on some level. I don’t pretend to know the perfect balance but when centers close in your home town and then the nearest facilities become 40 or 60 miles away, that is not ideal either. And again, the access is important, but the shrinking reach of our field in medicine due to declining revenue projections is the more critical component for our specialty long-term.

I completely understand that shorter means greater access to care in most spots around the world, but in America - our push to reduce costs is clearly affecting access in places and more broadly, de-emphasizing our role in cancer treatment - the later to me is actually the more critical aspect.

And if I’m honest, I did not see this on the agenda for the ASTRO meeting. The benefits of improved access for middle and low income nations was on the agenda - in prominent spots. But I looked through the daily schedule and did not see a discussion on the impact of rural access due to costs reductions and decreasing fractions in our market. I didn’t see talks on how to ensure investment and innovation in our equipment. It’s only real discussion was in the ROCR meeting where the issues are framed within a far more generalized “less revenue perspective” rather than an access to care / accessibility / innovation perspective.

Yet, beyond the structured meeting, the effects of fraction reduction and declining revenue was palpable. In conversations with industry, it is an open topic. Around the dinner table in the evening with physicians from Germany to Australia to Canada, they knew it was important to the US market. Amongst those along the back wall of the ROCR business meeting (the stand-in crowd from the overflow room), it was openly discussed as we tried to figure out how such a global change to Medicare billing might be truly implemented in a clinic setting. And around midnight on Monday, it moved to phones and texts as word started to spread that this advanced technology tool maybe soon gone. And yet, with all that ancillary discussion, within the primary agenda of the meeting, it was missing.

From my perspective, we need to continue to work to bring these topics to the forefront. We need to have real discussions regarding the need to balance our workforce against our trend to prioritize efficiency and that is why accepted the invite to help in shaping the conversations at a national level. In places, the pressures are bubbling to the top - think GenesisCare or now ViewRay. And as we’ve discussed you see efforts from our ASTRO leadership to turn the tide in their prior RO-APM approach and now in the ROCR model, but there is plenty of work to do.

My guess is few appreciated the ball gaining this much speed this quickly back 15 years ago. I did not. Five years ago - yes, but not 15 - and changes to healthcare policies take time. But now, this downward trend in fractions has incredible momentum and we’ve clearly been chasing the puck. Moving forward, we’ll need to adapt to maintain our leadership presence in shaping the future of oncology. If we don’t it will consolidate according to market pressures.

A quick story:

I’m a math guy but a simple one. Protons are on the other side of the current “restructuring”. Many of the large multi-room facilities have been restructured - both financially and structurally. Instead of 3 or 4 or 5 rooms, the main models are single room facilities. The model has adjusted. It adjusted to a fraction of the machines - say 1 in 4 was required.

Today, the math for linacs is similar. If you consider volumes and throughputs, the number of machines required is a fraction of what it once was. Mainly this is due to hypofractionation. My machines used to average ~25-30 under beam treating 250 patients in a year (back say 2005-2012). Math is simple: say 6 wks of treatment so 8.5 annual blocks is around 250 (8.5x30) per year. I’d see 275-300 consults and treat about 250 - ballparks.

Consider today - lets say the 30 treatments falls to 10 over the next decade - prostate and breast data essentially supports this number today. In contrast to before, that is 26 slots per year (52/2) so around 10 under beam is equivalent. But 10 per day is like 2 or maybe 3 hours for staffing, so lets just keep the number on the machine daily at 30. That same number now treats 3 years of patients each year. You need one machine where before it required three. Add in a more cautious evaluation of the proforma and one can easily move that to 40 per machine and you are starring at the proton restructuring figures. If the numbers today sit at 3500-4000, it could easily move to half.

Times are changing and the math looks similar to the proton adjustment to me.

As always, opinion of one - please comment if I’m wrong. I think things like adaptive planning and other concepts can limit throughput but if that is our path - WE MUST get new high dollar codes approved for the work. And small “add on” codes aren’t enough - it would require a 2x treatment code for the work / time.

I still believe we have a bright future as a specialty. The work we are doing is raising the bar for cancer patients. We just published 95%-96% cure rates for prostate cancer - not just in low risk but in more favorable intermediate risk disease. We demonstrate outstanding ability to avoid chemotherapy and systemic treatment for more than a year in patients with metastatic disease using radiation treatment and we do it at a fraction of the cost of the competing systemic approaches. We really are improving patient outcomes and providing great value. I do think the transition will be difficult in places. Some will feel the change much more than others, but I think if we begin to have more open conversations about what lies ahead for our field, the path forward will be easier.

Like I said, if you have suggestions on where and how this needs to happen - reach out. Happy to listen. I have some goals - we’ll see.

With the news of ViewRay, this one took a turn towards business. In the next few weeks, I hope to hit clinical meeting highlights. I had the opportunity to talk with about 20 true leaders in the field - some brilliant one on one conversations with people that are shaping the field. The smaller size of our field really is a blessing in ways. Hopefully I can pass along some of that experience within these tales.

Obviously we’ll come back and consider PACE-B and I’m going to try to piece together my thoughts on how I personally would transition a small rural setting practice to SBRT based on my experience of working in a single machine rural practice for 20 yrs paired with review of the data we have and my experiences learned in my first attempt. Thanks again for reading along as we strive for better.